You're probably here because J.M. Wilson showed up on a quote, policy document, or agent email, and you're trying to answer a basic question that should be simple but often isn't. Is this the insurance company? A broker? A wholesaler? And if you found older information online, you may also be wondering whether the company you're dealing with today is the same one those older profiles describe.

That confusion is reasonable.

J.M. Wilson has long operated in specialty insurance, which already sits outside the familiar direct-to-consumer model many buyers expect. Then came a major structural change in 2025, when the business moved from independent ownership into the Ryan Specialty platform. If you're a policyholder, an independent agent, or a software partner, that change matters because it affects who handles placement, how service flows, and what systems may change behind the scenes.

The practical question isn't just who J.M. Wilson was. It's what J.M. Wilson is now, and how that affects your next decision.

An Introduction to J.M. Wilson Insurance Company

A business owner often first encounters J.M. Wilson in the middle of a problem. A standard carrier won't write the account. The risk has unusual loss characteristics. The operation spans multiple exposures. Or the agent says, “We may need a specialty market for this.”

That's where J.M. Wilson Insurance Company, more accurately understood as J.M. Wilson Corporation doing business as J.M. Wilson Insurance Company, enters the conversation. It isn't best thought of as a household-name insurer selling simple policies straight to the public. It operates in the specialty side of the market as a managing general agency and surplus lines broker, which means it helps place business that standard markets often decline.

For buyers, that distinction changes expectations. You're usually not entering a direct relationship the way you would with a large personal lines brand. You're working through an independent agent, and that agent is using J.M. Wilson because the account needs market access, underwriting flexibility, or both.

Practical rule: If your risk is straightforward and easy to place, you may never need a specialty MGA. If your risk is unusual, that's when firms like J.M. Wilson become relevant.

The second point most buyers miss is that the company has changed identity in a meaningful way. Older summaries may describe it as an independent regional specialist. That background still helps explain its expertise, but it no longer tells the full current story. Today, any serious evaluation of J.M. Wilson has to account for its post-acquisition role inside Ryan Specialty and what that means for access, service structure, and technology.

A Century of Specialty Insurance Expertise

J.M. Wilson didn't appear overnight to chase a short-term market opportunity. It was founded in 1920 and built a long-standing position as a U.S. insurance broker and binding authority, with six offices nationwide over the course of its growth, according to this company profile.

That history matters because specialty insurance rewards accumulated judgment. In standard lines, the process is often built around highly repeatable submissions. In surplus lines and binding authority work, the account details tend to matter more, and edge cases show up constantly. A firm that has operated for more than a century has likely spent decades sorting through exceptions, carrier appetite shifts, and non-standard placements.

Why longevity matters in specialty markets

A long operating history doesn't automatically mean every policy is better or every process is smoother. It does mean the company had time to develop a reputation among independent agents who need help placing difficult risks. In practice, that usually comes down to three capabilities:

- Market familiarity: Knowing which carriers or facilities are worth approaching for unusual submissions.

- Underwriting discipline: Recognizing when a risk is placeable, when it needs restructuring, and when it should be declined.

- Operational repetition: Handling endorsements, certificates, renewals, and documentation in product categories that aren't always clean or uniform.

Those strengths are especially relevant in the product areas J.M. Wilson became known for, including transportation, property and casualty, marine, personal lines, and surety. Those are not casual product categories. They often involve layered exposures, stricter documentation, and more back-and-forth than buyers expect.

What worked for agents over time

Independent agents historically valued firms like J.M. Wilson for reasons that don't show up on a glossy overview page.

A good specialty partner usually helps when:

| Situation | What the agent needs |

|---|---|

| Standard carrier declines | Access to alternative markets |

| Risk has unusual operations | Underwriting review with nuance |

| Submission is incomplete | Guidance on what must be fixed |

| Coverage needs don't fit a standard template | Flexible placement options |

What doesn't work is treating a specialty MGA like a mass-market carrier. Buyers who expect instant direct binding with no underwriting questions often get frustrated. Specialty placement usually requires more documentation and more patience. That's not inefficiency. It's how complex risks get placed responsibly.

Who Is J.M. Wilson Today After the Ryan Specialty Acquisition

The most important fact about J.M. Wilson today is simple. It is no longer operating as the same kind of independent entity many older profiles describe.

In June 2025, Ryan Specialty signed a definitive agreement to acquire J.M. Wilson, and the acquisition was completed on July 1, 2025, with J.M. Wilson integrated into RT Binding Authority, Ryan Specialty's binding authority segment, as reported in Ryan Specialty's acquisition announcement carried by Nasdaq.

That changes the right answer to the question, “Who is J.M. Wilson?”

The current identity in practical terms

Today, J.M. Wilson is best understood as a legacy specialty brand operating within a larger specialty insurance platform. Its heritage still matters. Its product knowledge still matters. But from a business-strategy standpoint, it now sits inside a much broader organization with centralized governance, a larger distribution framework, and different operational expectations.

For agents, that usually means more than a logo change. It can affect:

- Market access: Broader platform resources can create additional pathways for placement.

- Operating model: Processes may become more standardized across the parent platform.

- Escalation paths: Service and underwriting decisions may follow different internal structures than before.

For policyholders, the day-to-day difference may feel subtle at first. Your independent agent still remains the key relationship in most cases. But behind the scenes, the entity supporting placement and service is no longer a standalone regional operator.

A lot of outdated content still describes J.M. Wilson as if the acquisition never happened. That's the biggest mistake buyers can make when evaluating the company in 2026.

What the acquisition means for specialty buyers

This shift can be a positive if you need specialty expertise backed by larger infrastructure. It can also create transition friction. Both things can be true at once.

If you're trying to place a hard-to-write contractor, transportation, or non-standard liability account, it helps to work with an intermediary that understands surplus lines structure. For businesses dealing with unusual field operations, this primer on securing specialty contractor insurance is useful because it explains why admitted markets sometimes step back and why excess and surplus access becomes necessary.

The key trade-off is straightforward:

| Potential benefit | Possible friction |

|---|---|

| Larger platform support | Integration changes |

| More formal governance | Less informal flexibility |

| Broader specialty network | Process adjustments during transition |

That's the lens I'd use. Don't ask whether J.M. Wilson still has value after the acquisition. Ask whether its specialty capabilities now fit your needs within a larger Ryan Specialty environment.

Types of Insurance Offered Through J.M. Wilson

J.M. Wilson operates in areas where standard carriers often say no, or say yes only after narrowing coverage so much that the policy no longer solves the problem. That's why its product mix matters more than its brand familiarity.

The company has been described as a managing general agency and surplus lines broker with approximately $29.7 million in gross written premium in 2023, focused on commercial transportation, P&C brokerage, professional liability/E&O, marine, personal lines, and surety, according to this industry profile.

Where J.M. Wilson tends to fit best

This isn't a mass-market menu. It's a specialist's lineup. Buyers should think in terms of problem accounts, not broad consumer categories.

-

Commercial transportation

This often fits businesses with vehicles, cargo exposures, or operating patterns that make standard underwriting less comfortable. Long-haul, specialized hauling, or layered operational risk can push an account into specialty review. -

Property and casualty brokerage

This is the wide middle ground where many unusual commercial placements live. The issue might be occupancy, claims history, operational complexity, or an exposure that doesn't fit a standard box. -

Professional liability and E&O

This comes into play when a business sells advice, design, expertise, or services that can trigger financial harm allegations rather than straightforward bodily injury or property damage claims.

Product lines buyers often misunderstand

Some categories sound familiar but work differently in specialty markets.

| Coverage area | What makes it specialty-oriented |

|---|---|

| Marine | Inland or specialized marine exposures often require niche underwriting |

| Personal lines | High-complexity homes, assets, or risk profiles may need non-standard placement |

| Surety | Bond needs can be highly specific and tied to business qualifications or obligations |

A common mistake is assuming “personal lines” means broad direct-to-consumer home and auto. In a specialty MGA setting, it usually means something narrower or more complex than ordinary household coverage.

How to tell whether your account belongs here

Ask these questions:

-

Has a standard carrier already declined the risk?

If yes, J.M. Wilson may be relevant. -

Does the account involve unusual operations or documentation?

Specialty intermediaries are often better suited for those submissions. -

Do you need coverage structure more than brand recognition? Buyers sometimes focus too much on a famous insurer name and too little on whether the policy fits the exposure.

Specialty placement works best when the insured and agent are honest about the risk. Clean submissions matter, but complete submissions matter more.

What doesn't work when using a specialty market

Three habits create avoidable problems:

- Forcing a standard-market narrative: If the exposure is unusual, trying to package it as ordinary usually delays placement.

- Submitting sparse information: Specialty underwriters often need details up front. Missing operational data slows everything down.

- Shopping purely on price: In hard-to-place business, narrow coverage can become expensive the moment a claim hits.

J.M. Wilson makes the most sense when the goal is not “find me the cheapest policy,” but “find me a market that can write this correctly.”

Navigating the Claims and Customer Service Process

The service model matters as much as the product. With a specialty MGA structure, many policyholders assume they should contact the brand on the paperwork directly for everything. Sometimes that's appropriate, but in most cases your independent agent remains your first and best point of contact.

That's because the relationship usually involves three parties: the insured, the retail agent, and the specialty intermediary. J.M. Wilson sits in the middle of that chain for placement and service support, while the policyholder often experiences the relationship through the agent.

Who should handle what

A simple breakdown helps:

- Your agent: Best first contact for claims reporting guidance, policy questions, endorsements, certificates, and renewal strategy.

- J.M. Wilson or platform service team: Often involved in processing, market coordination, underwriting communication, and specialty workflow support.

- Carrier or claims administrator: May ultimately adjust or administer the claim depending on the policy structure.

This setup can feel slower if you expect a direct-call-center model. But it often works better for specialty business because your agent can frame the issue correctly before it reaches underwriting or claims.

When a specialty claim or service request gets messy, the agent's ability to organize facts and documentation often matters more than the speed of the first email.

What policyholders should expect

Don't treat specialty service like online retail support. You may need to provide schedules, signed forms, loss details, or operational clarification before anything moves.

That's especially important in claims situations. Homeowners and small business clients who haven't dealt with a disputed claim before may benefit from outside perspective on communication and documentation. This guide on advice for homeowners on insurance negotiation is useful because it outlines how to approach insurer discussions without making the process more adversarial than necessary.

Service quality also depends on channel consistency. If your agency uses multiple touchpoints, the basics in this article about omnichannel customer experience apply well to insurance service. Clients get frustrated when they repeat the same issue across phone, email, and portal messages with no continuity.

What works and what doesn't

A practical comparison:

| Works | Usually backfires |

|---|---|

| Reporting issues through your agent with full documentation | Sending fragmented updates to multiple contacts |

| Asking who the actual claims administrator is | Assuming the MGA itself adjusts every claim |

| Keeping all policy records organized | Looking for documents after a loss occurs |

If you're insured through J.M. Wilson, the best move is usually simple. Start with the agent who placed the account, ask for the exact reporting path, and keep communication tight and documented.

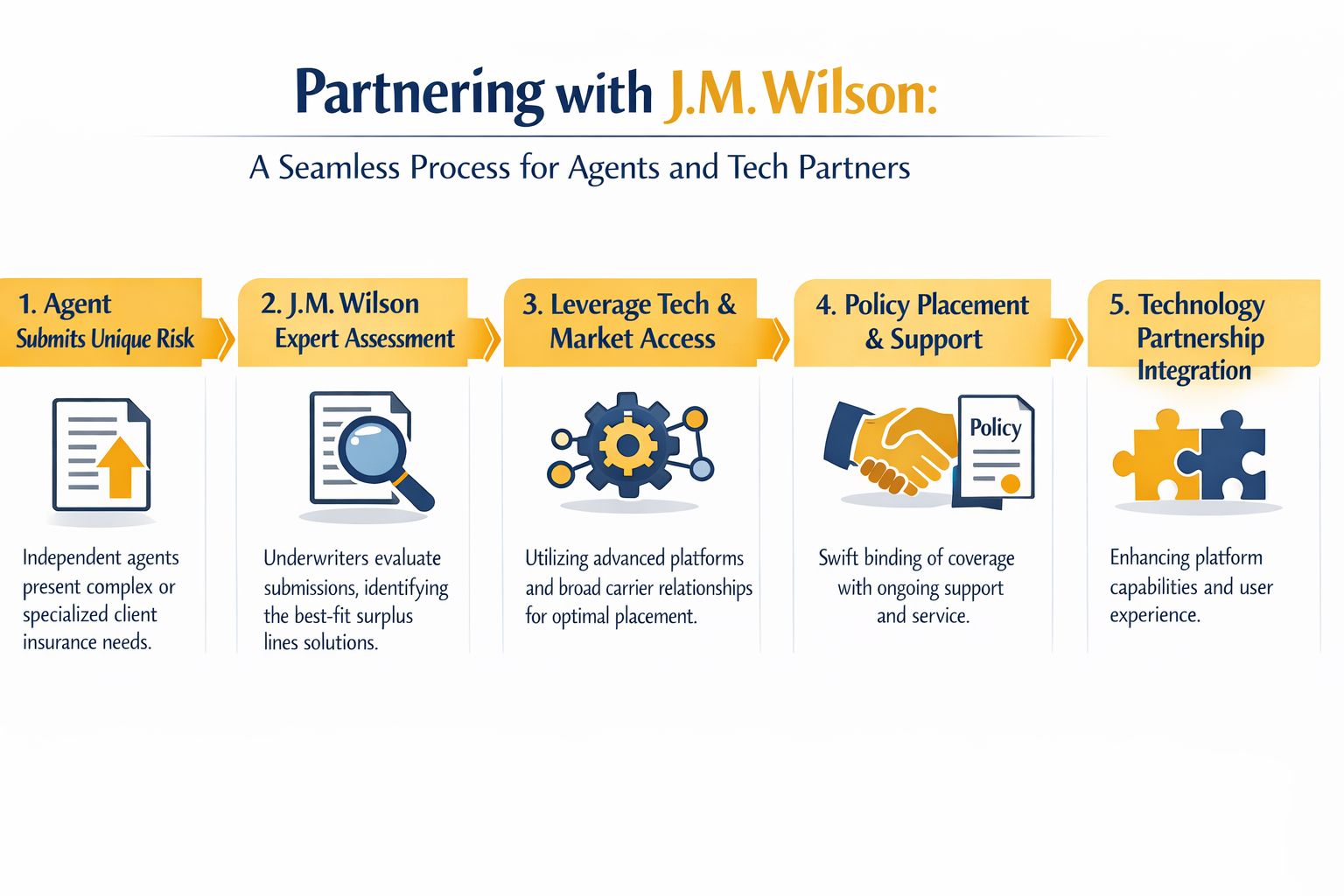

A Guide for Agents and Technology Partners

The acquisition yields its most immediate operational impact on independent agents, agency principals, software vendors, and internal systems leads. They shouldn't evaluate J.M. Wilson only as an underwriting relationship, but as a changing integration environment.

Following the acquisition, J.M. Wilson's systems are being integrated into Ryan Specialty's technical governance model, and stakeholders should anticipate changes to APIs, data schemas, and authentication methods over a typical 12 to 24 month harmonization period, according to Ryan Specialty's acquisition notice.

What agents should do during the transition

If your agency uses a portal manually, you may feel this only as small login or workflow changes. If your team depends on exports, comparative raters, document sync, or CRM automation, the impact can be larger.

Here's the practical checklist I'd use:

-

Audit dependencies first

Identify every place your team relies on J.M. Wilson data, document delivery, credentials, or submission workflows. -

Map fields before problems appear

If you import data into an agency management system, note which fields are critical and where mismatches would break downstream reporting. -

Prepare for authentication changes

Login methods and user permissions often change during platform integration. That can interrupt service if no one owns credential governance.

What technology partners should engineer for

The wrong approach is assuming current workflows will remain stable because the front-end experience still looks familiar. The better approach is to build for drift.

Build integrations as if field names, endpoints, and login methods can change in stages. Because in acquisitions like this, they often do.

A resilient setup usually includes:

- Version tolerance so minor schema changes don't break the whole workflow.

- Structured error logging so failed requests are visible immediately.

- Fallback handling for document delivery, quote retrieval, or policy status sync.

- Human review triggers when the system sees unexpected values or missing required fields.

For agencies that treat CRM and workflow tools as separate from distribution strategy, that separation won't hold up well. This perspective on CRM and digital marketing is relevant because customer communication, renewal outreach, and submission operations increasingly depend on the same data quality.

The real trade-off after integration

There's a familiar pattern in specialty acquisitions.

| Upside | Operational cost |

|---|---|

| More consistent governance | Temporary workflow disruption |

| Better long-term standardization | Short-term retraining |

| Broader enterprise infrastructure | Need for monitoring and adaptation |

Agents and tech teams that do best during this period don't wait for a hard failure. They test, monitor, and confirm assumptions continuously. In specialty insurance, one broken field mapping can create a quoting issue. One broken authentication flow can stall service entirely.

Is J.M. Wilson the Right Choice for Your Insurance Needs

J.M. Wilson is a fit for buyers who need specialty market access, not for everyone shopping for insurance.

If your business has a complicated transportation exposure, unusual property profile, non-standard liability concern, or another account that standard carriers keep declining, J.M. Wilson can make sense. The same is true if your independent agent needs a wholesale or MGA partner that knows how to work through harder submissions rather than forcing a standard-market template onto a non-standard risk.

Best-fit buyer profile

J.M. Wilson tends to fit well when:

- Your risk is hard to place

- You're comfortable working through an independent agent

- You care more about market access and fit than a familiar consumer brand

- You understand that specialty underwriting usually requires more documentation

It's less likely to be the right path if your needs are simple, easily handled by admitted carriers, or better served through a direct retail insurer with an efficient self-service model.

The clearest way to decide

Ask your agent two questions.

First, is the account being sent to J.M. Wilson because the risk is specialized? Second, has the Ryan Specialty integration changed any service, portal, or claims workflow you should know about right now?

If the answers point to a real specialty need and a competent service path, J.M. Wilson remains a serious option. If the account is ordinary and your only goal is convenience, there are usually easier routes.

For businesses trying to improve the client side of these interactions, the broader lessons in how to improve customer experience apply well. Even in specialty insurance, the firms that communicate clearly tend to earn the most trust.

If your business needs better digital infrastructure around complex customer journeys, including insurance workflows, portal experiences, CRM alignment, or custom web applications, Up North Media can help. Their team works with growing businesses that need practical technology and marketing systems, not generic advice.